%201.webp)

02

AI Snaps

.svg)

.svg)

01

Our Work

03

About Us

05

Contact Us

06

Client Success

07

Blogs

08

Careers

Book A Call

Need Help In Building Your Brand?

Click the button below & book a call with our founder directly.

Rishabh Jain

Managing Director

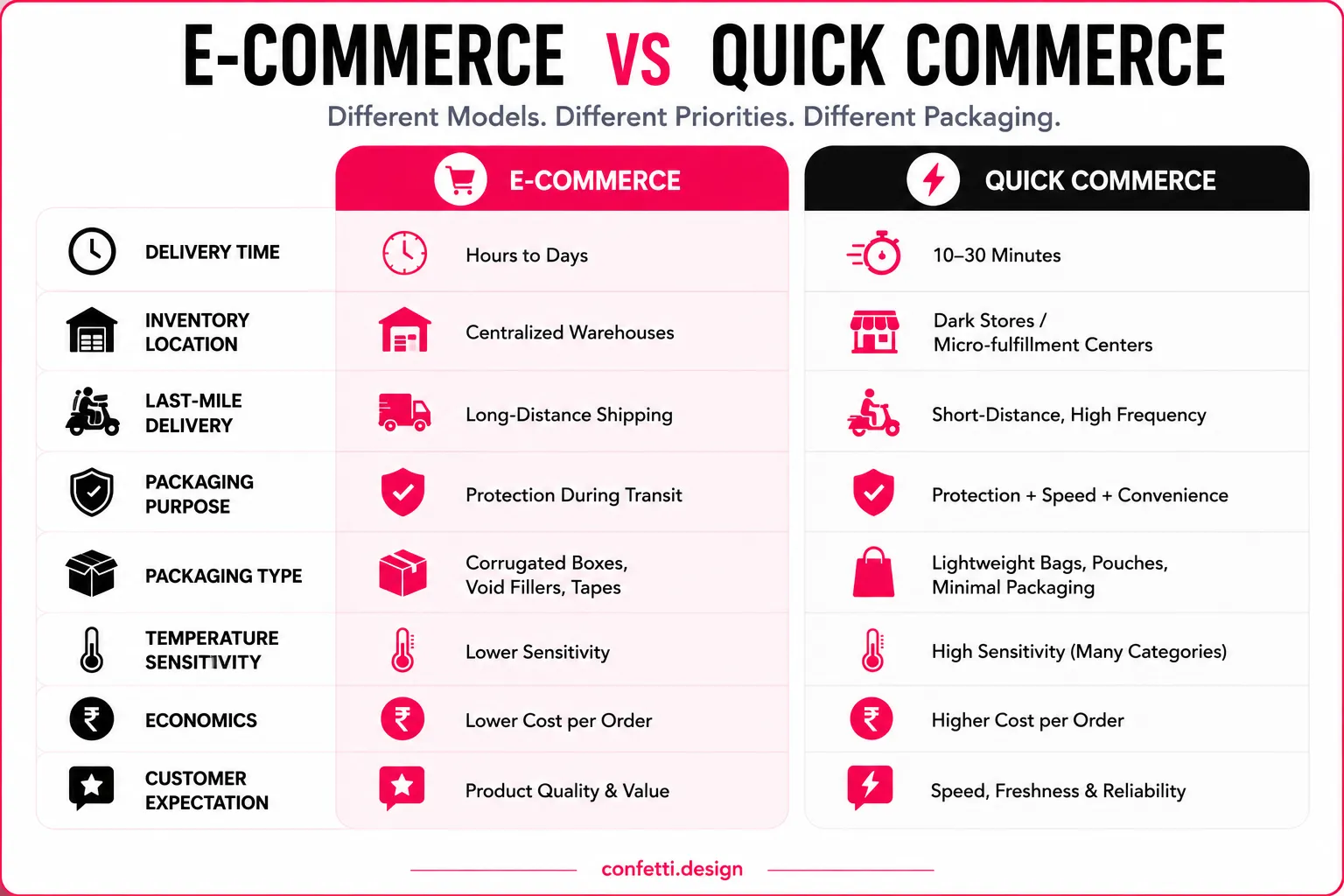

Ecommerce and quick commerce are not faster and slower versions of the same thing. For brands, who want to sell, they are fundamentally different right from their packaging needs to their strategy.

This Confetti blog covers what actually is important for your brand: packaging, SKU strategy, margins, and consumer behaviour on ecommerce and quick commerce and how you need to plan to get the best results.

Ecommerce and quick commerce both are inherently different shopping behaviours.

🛒Ecommerce is where consumers go to browse and decide.

🛒Quick commerce is where they go when they've already decided.

That distinction changes channel strategy, packaging, SKU selection, margins, and brand positioning.

Ecommerce is where consumers browse, compare, and make considered decisions, usually with delivery fulfilled within 1–5 days.

When someone opens Amazon or Flipkart, they're usually in one of two modes: they know the category but not the brand, or they're actively comparing options before committing. They'll read ingredient lists, scroll reviews, check competitor pricing, and switch tabs.

The path from intent to checkout can take minutes or days.

This is why platforms like Amazon, Flipkart, Myntra, Meesho, and brand-owned D2C websites have deep catalogs, detailed product pages, recommendation engines, and review systems.

The entire architecture is designed to support deliberation.

A strong product listing with optimised titles, A+ content, accurate attributes, and review volume, can surface a new brand to a consumer who didn't know it existed an hour ago. Discovery is a real outcome here.

For packaged goods brands specifically, ecommerce offers something quick commerce doesn't: the space to tell your story. A well-built product page can carry origin claims, certifications, usage instructions, comparison charts, and brand narrative.

Quick commerce is the delivery of goods: usually groceries, personal care, or household essentials within 10 to 15 minutes, fulfilled through a network of dark stores positioned within 2–4 km of residential demand clusters.

The consumer on Blinkit or Zepto is not browsing. She already knows she needs eggs, a specific shampoo, or a packet of the chips her kids have been asking for. The job is retrieval. The faster the app gets her there, the better the experience.

On quick commerce, you're not winning someone over, you're being available at the exact moment they need you. If your brand isn't listed, or your SKU is out of stock, the sale goes to whoever is.

The model is about curation, not volume. A single dark store usually carries 2,000–5,000 SKUs. Compare that to millions of listings on an ecommerce marketplace.

As a brand you must be aware of the operational differences between these two channels. Let's see how those differences demand from a brand.

Each dimension is a strategic constraint that shapes decisions around pricing, packaging, inventory, and marketing spend.

🔶Delivery time is the most visible difference, but it's the least instructive for brand strategy. Swiggy Instamart brought its average delivery time down from 17 to 13 minutes. The platforms are in an active race to compress that window further.

For brands, this means if your product isn't physically in a dark store, it doesn't exist for that consumer at that moment. No algorithm can compensate for an empty shelf.

🔶Product range is where the difference really shows for brands. Ecommerce carries unlimited SKU depth, a brand can list 40 variants across sizes, flavours, and formats without any gatekeeping from the platform.

In quick commerce, dark stores are small, inventory turnover is everything, and category managers are ruthless about what earns shelf space. Getting your top two or three SKUs listed is the entry point. Keeping them stocked and turning is how you stay listed.

🔶Consumer intent shapes everything from how your product page is built to how much copy you can realistically put on a pack. An ecommerce shopper will read.

A Blinkit or Zepto shopper will glance. Your product packaging needs to communicate differently in each context, which is a packaging and content problem, not just a channel problem.

🔶Infrastructure determines where your operational risk sits. Centralised warehouses mean one point of failure, but also one point to manage.

Dark stores mean your product needs to be reliably distributed across dozens of micro-locations across a city, with each location managing its own inventory independently. Restocking coordination, expiry management, and demand forecasting all get more complex at this level of distribution granularity.

🔶Platform economics differences are huge. Ecommerce commissions usually sit between 15–30% depending on category.

Quick commerce commissions ranges between 8%–20% and that's before factoring in other fees. Blinkit charges ₹25,000 per SKU per state for onboarding (will be added to your ad wallet).

For an early-stage D2C brand, this isn't a small line item, it's a go/no-go decision.

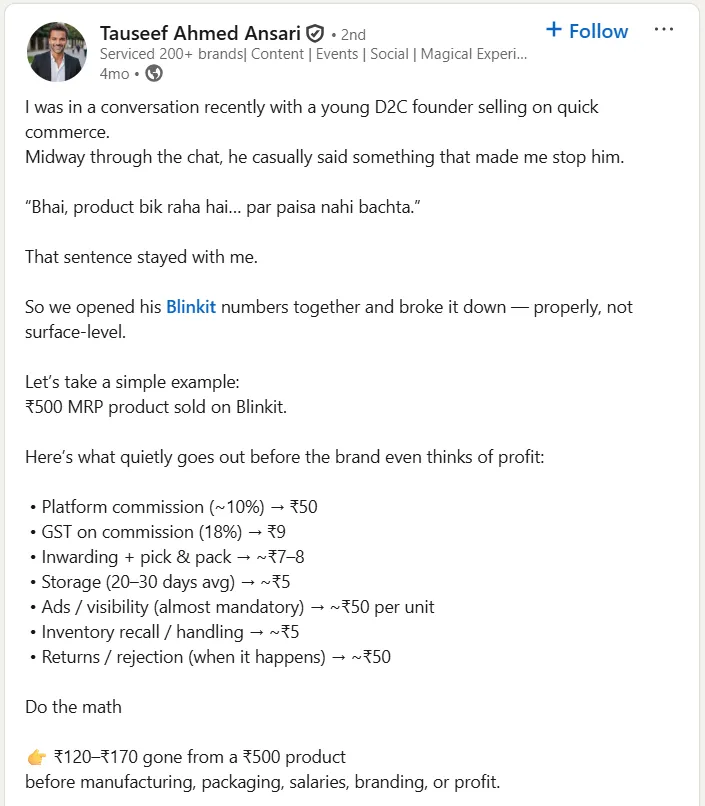

📌You can see how your unit economics looks like by observing this LinkedIn post, which explains about what is the actual cost of selling on Blinkit.

🔶Brand visibility mechanics are structurally different. On ecommerce, you invest in content: keyword-optimised titles, A+ pages, review acquisition, and search placement. A well-built listing compounds over time, and organic rank is a real asset.

On quick commerce, visibility is driven: whether you're in stock, how fast your SKU turns, and whether you're paying for placement on the app's homepage or category shelf.

Brand equity helps, but a brand with mediocre content and reliable restocking will consistently outsell a brand with beautiful listings that can't maintain dark store fill rates.

💡Ecommerce rewards brand building. Quick commerce rewards operational discipline. Most brands need both.

The phrase "getting listed" means something entirely different depending on the channel you're talking about.

Amazon India carries over 170 million product listings. Flipkart is comparable in scale. When you list a new packaged food SKU on either platform, you are invisible, until you earn visibility through content, advertising, or review volume.

This is the defining challenge of ecommerce: the shelf has no limit. Your product competes with hundreds of alternatives for the same search query.

A consumer searching "protein granola bar" on Amazon may see sponsored results, then Amazon's own private label, then established brands with thousands of reviews before your listing appears, if it appears at all.

Visibility on ecommerce is earned through:

On ecommerce, a brand with better content can consistently outrank a brand with a better product. A challenger brand with a well-optimised listing, strong packaging imagery, and a few hundred verified reviews will outperform a superior product with thin content and low review velocity.

You're building for ecommerce, content infrastructure is as important as the product itself.

For new D2C brands, this means ecommerce requires sustained investment before it yields returns. The discovery opportunity is real, a consumer who didn't know your brand exists can find it, evaluate it, and buy it within a single session. But getting to that moment of discovery takes time and budget.

On Blinkit or Zepto, a consumer searching for muesli might see four or five options. That's it. The dark store near her carries what it carries, ranked by how fast those products sell.

If your brand is one of those four or five options, you are already a primary contender, the curation has done part of the brand-building work for you.

But staying on that shelf is a different challenge. Quick commerce platforms rank visible SKUs by three primary factors:

A brand that lists and then lets fill rates slip will see a dip in rankings, visibility shrink, and eventually face delisting, without any visible signal to the consumer.

Consumers won't see a message saying your product is out of stock. Consumers will just see your competitor, and buy that instead.

Approximately 50% of quick commerce consumers will switch to a competing platform entirely if their preferred brand is unavailable. Stockouts don't just cost you a sale; they actively push acquisition volume to competing platforms.

📌4700BC, the gourmet popcorn brand, is the clearest example of what it looks like when a brand understands quick commerce's curated shelf model. They built for velocity, tight SKU range, strong dark store fill rates, and consistent in-app advertising and quick commerce now generates the majority of their revenue from the channel.

They won by being reliably present within a small, curated set.

Talk to Confetti experts about getting marketplace-ready

Book A Call

The same person who spends 20 minutes comparing protein bars on Amazon will spend 90 seconds on Blinkit or Zepto getting the one she already buys.

Same consumer. Same category. Completely different behaviour and if your brand strategy doesn't account for that, you're solving for the wrong problem on at least one of these channels.

A consumer opens Amazon with a vague intent, "I need a face moisturiser" or "looking for a healthy snack for kids" and the platform immediately presents her with choices she wasn't necessarily shopping for.

She scrolls, filters, clicks into three or four listings, reads ingredient lists, checks the Q&A section, looks at the 3-star reviews specifically (because those are honest), and compares two finalists on price and shipping time. Then she adds one to her cart and closes the app.

She comes back two days later and buys it. Sometimes.

This extended, non-linear journey is actually an opportunity, if your brand is set up to use it.

Every element of your product listing participates in that process: the primary image, the title, the bullet points, the A+ content, the review count, the brand story section.

Long-form brand narrative has real value here. If your product has a meaningful origin story, a certification worth highlighting, or a formulation that genuinely differentiates it from cheaper alternatives, ecommerce is where you make that case.

A consumer who has spent time on your listing and understands why your product costs more will convert at a higher rate and return more reliably than one who bought on price alone.

This also means that ecommerce is where you build the brand trust that makes everything else possible downstream.

On Blinkit or Zepto, she opens the app, types "Epigamia Greek yogurt" or "Minimalist 10% niacinamide," sees it in stock, taps add, goes to checkout.

The whole interaction takes under 2 minutes. She already knows what she wants, she's done this before.

For brands this implies quick commerce is not where consumer trust is built. It's where it is acted on.

Although people go with familiarity, quick commerce is also a place where impulse buying happens and people try new products and even new brands.

A consumer who opened Blinkit for curd can leave with a snack brand she's never heard of, if the thumbnail is compelling and the price point is low enough to reduce purchase risk or it has something unique to offer.

📌For example, BlinkIt’s instagram handle regularly features users who find interesting and new options on blinkit. This helps new brands to get visibility through social media which is an added advantage.

The way a consumer encounters your product on Amazon and the way they encounter it on Blinkit is not just different in speed.

They are different in screen size, visual context, decision time, and physical delivery conditions.

On ecommerce, your consumer never sees your packaging in person before they buys but the photography and content system around it does the actual selling.

This means your ecommerce packaging needs to support a multi-image narrative.

Every face of the pack, every callout, every certification badge needs to be photographable and legible at the image sizes platforms use.

You know how some packaging looks amazing when you’re holding it, like with embossed textures or foil accents but then you take a photo and it just looks flat and lifeless? Same goes for matte finishes; they can seem dull unless you nail the lighting just right.

The first physical touchpoint in an ecommerce purchase is the unboxing moment and it arrives days after the buying decision.

Secondary packaging (the shipping box, tissue paper, printed inserts, thank-you cards) carries the full weight of that first impression. This is where brand loyalty is either reinforced or quietly eroded.

If a premium product shows up in a plain brown box with no thought given to the unboxing experience, it creates a disconnect between how the brand sells itself online and how it actually delivers. And people notice that gap.

Structural packaging must account for multi-handoff courier logistics, across warehouses, hubs, and last-mile delivery over distances that can span hundreds of kilometres.

On quick commerce, your primary packaging is the shelf unit.

The consumer sees your product front face as a thumbnail on a mobile screen and makes a tap-or-scroll decision in under three seconds.

At that size, what actually registers is:

Fine typography, intricate illustration, and detailed ingredient callouts are invisible. A cluttered front face one that tries to communicate too much, will lose to a cleaner design with stronger colour hierarchy and a readable brand mark.

Secondary packaging on quick commerce is a different challenge. It needs to survive a two-wheeler delivery over 2–3 km of urban roads.

Similarly, packaging that's appropriate for shelf retail may not protect the product through the road vibration and bag compression of a delivery run for Zepto.

Pack size is where the most expensive mistakes happen. Dark stores allocate shelf space by velocity.

A 5 kg bag of atta that sells reliably through a kirana store is a poor Q-commerce SKU, it's slow to move, occupies disproportionate shelf space, and is difficult to handle on a delivery bike. A 1 kg or 2 kg pack with a fast reorder rate fits the model.

Your ecommerce SKU lineup and your Q-commerce SKU lineup should be different by deliberate design, as a channel strategy decision made before you brief your packaging design studio.

What strong SKU architecture actually looks like:

A premium snack brand that sells a 400g sharing pack on Amazon and a 30g single-serve on Blinkit is serving the same consumer in two distinct need states.

The consumer buys the big pack when stocking up.They buy the single-serve when they wants one now. Both SKUs are intentional.

📌At Confetti, packaging for ecommerce and quick commerce is not the same brief. Before we start working on the designs, we audit existing platform specific requirements and what will work best.

Before you decide where to invest, you need to understand what each platform actually takes: in commission, in fees, in advertising spend, and in the operational overhead that doesn't appear in any platform rate card.

Platform commissions on ecommerce are usually between 15–30% of product value, varying by category.

On top of that, brands serious about scaling on Amazon or Flipkart are spending an additional 5–15% of GMV on advertising: sponsored products, display placements, and brand campaigns, to build and maintain visibility in competitive categories.

The core economic advantage of ecommerce is reach. A single optimised listing can serve every city in India simultaneously, from a centralised warehouse. There's no per-city, per-state listing fee. The infrastructure investment is made once, and the addressable market is national from day one.

D2C ecommerce websites change the commission equation significantly. Without a marketplace taking a cut, brands pay only payment gateway fees (usually 1.5–2%) and logistics costs.

The margin structure is better. The cost is customer acquisition brands are spending on Meta ads, Google campaigns, and influencer partnerships to drive visitors.

Customer acquisition costs for D2C websites in India are commonly set between ₹300–800 per first-time buyer depending on category, which can take multiple repeat purchases to recover.

The long-term upside of ecommerce is that a well-optimised listing with strong review velocity can drive organic sales for years with minimal ongoing spend.

Quick commerce's fee structure is categorically different.

Platform commissions range is between 8–20% of product value, roughly double what ecommerce platforms charge. Blinkit charges ₹25,000 per SKU per state as a listing fee, payable upfront before a single unit moves (this will be transferred to an ad wallet).

Brands targeting 3-4 states with five SKUs are looking at ₹3–5 lakh in listing fees before operations even begin. Advertising budgets for meaningful visibility: homepage placements, category banners, search ads, ranges ₹10–20 lakh per month on major platforms.

Swiggy Instamart also mandates minimum weekly purchase orders, usually in the ₹2,000–5,000 range per dark store, which creates a baseline inventory commitment regardless of actual sell-through.

Both, but the sequence, the SKU mix, and the success metrics should be different for each and getting that wrong is expensive.

The two most common mistakes we see:

Here's a framework for thinking through channel fit before you commit a budget.

Evaluate your brand against five dimensions:

No brand scores cleanly in one column. The scorecard tells you where to start and where to invest more heavily, not where to be exclusively.

🛍️Quick commerce is well-suited for:

🛍️Ecommerce is better suited for:

The category boundaries are not fixed.

A supplement brand that has built significant awareness through social and ecommerce can successfully transition top SKUs to quick commerce once consumers are searching for it by name.

Running both channels from launch makes sense in specific circumstances:

In most cases, the problem isn't the platform, the category, or even the product. It's upstream in the packaging, the pack size, or the brand visibility strategy that was never built for these channels in the first place.

Many brands by the time they reach us, have already spent on listing fees and platform advertising.

Our job, at that point, is partly to fix what's there and partly to explain why the sequencing went wrong, so it doesn't happen again with the next SKU.

Most packaging is designed to look good in a photoshoot or on a physical shelf.

Those are not the same design problems as performing at 200×200 pixels on a mobile screen, inside a grid of five competing products, viewed by a consumer who has already decided what they want and are scanning to find it fast.

We design primary packaging with Q-commerce as a primary context, which means front-face hierarchy, brand name legibility, and colour contrast are evaluated at thumbnail scale before we finalise anything at print size.

Before recommending a redesign, we audit what exists.

A targeted label intervention is faster and cheaper than a full redesign, and we'll always tell you which one the situation actually calls for. Our packaging design work is built around this kind of diagnostic-first approach.

We review pack sizes and SKU architecture before any design brief is written.

A brand that prints 10,000 units of a 750ml personal care product and then tries to list it on Zepto is going to have a problem because the format wasn't designed for a delivery bag or a dark store shelf allocated by velocity.

We advise on format and sizing before you commit to production. We look at what category managers on each platform actually stock, what pack sizes move at the velocity needed to maintain listing, and how your proposed format performs against competitive SKUs in the same dark store.

For ecommerce, the same audit runs in the other direction, identifying where larger formats, bundles, or value combos can improve per-order economics and encourage repeat subscription behaviour.

We support brands through the full onboarding process, seller registration, catalog creation, image compliance, and platform negotiation across all major Q-commerce channels.

The documentation requirements are different across Blinkit, Zepto, and Swiggy Instamart, and the timelines are longer than most brands consider.

At Confetti, packaging for ecommerce sales is designed and tested based on the consumer behaviour.

On ecommerce, we build the identity systems, A+ content architecture, product photography direction, listing copy, brand storytelling, and the visual consistency that turns a first-time buyer into someone who searches for you by name six months later.

What is the main difference between ecommerce and quick commerce?

Ecommerce delivers a wide catalog over 1–5 days and caters to planned, discovery-led purchases. Quick commerce delivers a curated set of high-demand products in 10–30 minutes and caters to urgent, need-state purchases.

For brands, the key difference is not just speed, it's consumer mindset, digital shelf mechanics, packaging requirements, and platform economics, all of which differ fundamentally between the two channels.

Can a brand be on both ecommerce and quick commerce at the same time?

Yes, and most mature brands should be. But the strategy for each channel must be separate. Your SKU lineup, pack sizes, packaging design, and success metrics will differ. Ecommerce builds brand awareness and serves considered purchases.

Quick commerce converts high-intent consumers quickly. Running the same product at the same price with the same packaging across both channels is not an omnichannel strategy, it's an oversight.

Which products work best on quick commerce platforms?

High-velocity, impulse-friendly, daily-use products perform best: snacks, beverages, personal care, OTC health products, baby essentials, and premium staples.

Products that are heavy (over 5–10 kg), fragile without specialized packaging, require consumer education before purchase, or carry very low gross margins tend to underperform on quick commerce due to the channel's economics and physical delivery constraints.

How do packaging requirements differ between ecommerce and quick commerce?

In ecommerce, packaging is experienced through photography, multiple angles, lifestyle images, and A+ content carry the brand story. In quick commerce, primary packaging must read clearly as a mobile thumbnail at very small sizes.

Brand name, variant, and key claim must be legible on screen. Pack sizes also differ: trial and single-serve formats outperform bulk packs on quick commerce platforms.

Is quick commerce replacing ecommerce in India?

No, they are complementary channels serving different consumer needs. Quick commerce has captured over two-thirds of e-grocery orders in India, but ecommerce continues to dominate in fashion, electronics, considered purchases, and non-metro markets.

Most analysts expect both to grow simultaneously through 2030, with quick commerce expanding into new categories and ecommerce deepening its reach into Tier-2 and Tier-3 cities.

How do I get my brand listed on Blinkit or Zepto?

Blinkit's seller portal allows direct applications, with usual review timelines of 2–4 weeks if documentation is complete. Zepto and Swiggy Instamart operate more curated onboarding processes that can take 4–10 weeks.

You will need: business registration documents, FSSAI license (for food brands), product catalog with images, pricing, and GST details. Working with an experienced onboarding partner reduces friction significantly.

What does "digital shelf" mean in quick commerce, and why does it matter?

The digital shelf in quick commerce refers to the limited set of products visible to a consumer when they search for a category on platforms like Blinkit or Zepto.

Unlike ecommerce, quick commerce apps usually surface 3–10 options per query. If your brand is not in that set or is out of stock, you are functionally invisible, regardless of how strong your brand equity is elsewhere.

Want strategic branding and packaging like this for your business?

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.svg)

.webp)

.svg)

.webp)

.webp)